2301 Harrisburg Pike

Lancaster, Pa 17601

717-898-3278 or 717-490-6489

A.L.M. Tax Service

For Life's Taxing Moments...

2301 Harrisburg Pike

Lancaster, Pa 17601

717-898-3278 or 717-490-6489

For Life's Taxing Moments...

Owned and operated by William J Waters CPA, CFP, MBA). ALM Tax Service has the expertise and experience to handle all tax preparation and planning for individuals and small businesses. We also offer payroll services, bookkeeping services, and financial consulting. William J Waters is a CPA and is admitted to practice before the Internal Revenue Service. He is licensed in the State of Pennsylvania and Illinois.

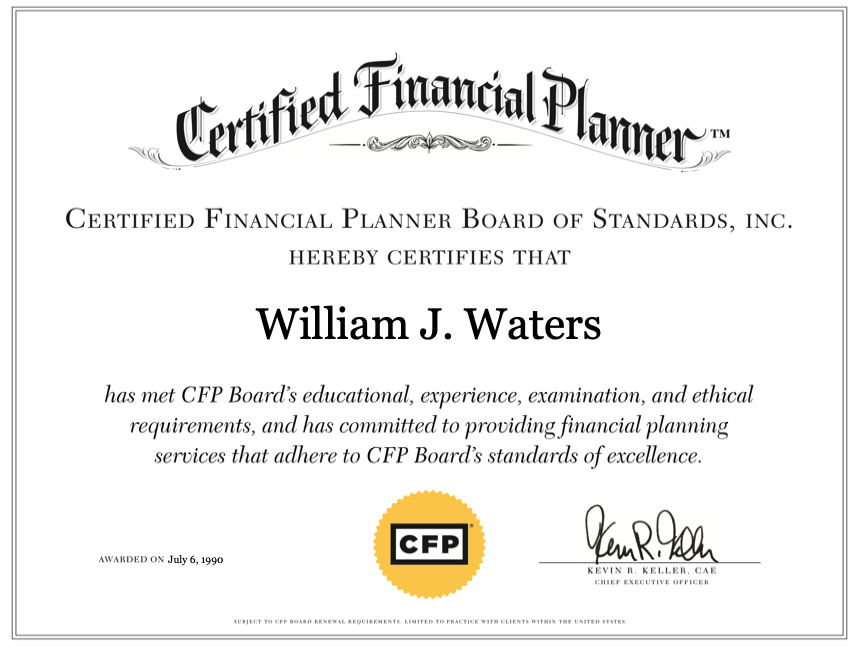

William J Waters has met Certified FInancial Planner Board's educational, experience, examination, and ethical requirements, and he has committed to providing financial planning services that adhere to CFP Board’s standards of excellence.

Members of the staff at ALM Tax Service include:

Barry Fink

Skills developed over a 40 year career in large fortune 500 companies, primarily in the printing industry:

Megan Waters

Megan is a graduate of Millersville University with a BS in Accounting and has been preparing individual tax returns for over 5 years.

ALM Tax Service is located in Lancaster, Pa at 2301 Harrisburg Pike in the Golden Meadows Business Park behind Reality Church.

Call our office at 717-898-3278 or 717-490-6489 if you have a tax question or have a need for our services.

Business hours during tax season (Jan 15th - April 15th) are:

10a-7p Monday thru Thursday

10a-5p on Friday

10a-12p on Saturday

All other hours are by appointment

The qualified business income deduction (QBI) allows eligible self-employed and small-businessowners to deduct up to 20% of their qualified business income on their taxes.

WASHINGTON – Millions of Americans with children will see more money in their bank accounts starting in July.

The Treasury Department and the Internal Revenue Service will begin sending monthly advance payments of $250 or $300 to low- and moderate-income families under the newly expanded Child Tax Credit starting July 15.

The payments will continue on a monthly basis through December, and most eligible families will receive them via direct deposit, senior administration officials said Sunday. Families that don’t have direct deposit will receive the payment either as a paper check or a debit card.

Monthly advance payments under the Child Tax Credit are the result of President Joe Biden’s American Rescue Plan, a $1.9 trillion coronavirus-relief package that Congress passed in March. The law extended the tax credit, boosted the amount that eligible families could receive and provided for half of the money to be made available in monthly installments through December.

Under the new law, families claiming the credit will receive up to $3,000 per qualifying children between ages 6-17 or $3,600 for each child younger than 6. Previously, the tax credit was up to $2,000 per qualifying child under age 17.

The payments will be sent automatically, so eligible taxpayers who have already filed their taxes don’t need to take any other action. The Treasury Department estimates that 80% of eligible families will get the payments via direct deposit.

An online portal will be set up so eligible taxpayers who prefer to receive the credit when they file their income taxes will have the opportunity to opt out of the advance payments. Another online portal will be created so taxpayers may provide the IRS with updated information about changes in their income, filing status or their number of qualifying children.

It is important to take action if you do not want these payments to be made in advance. If you receive these payments in advance they will reduce the credit that you are entitled to when you file your taxes – so they will have an impact on your refund amount for the 2021 tax year.

This is NOT a stimulus payment it is an ADVANCE on the child care credit that you normally get when you file your tax return.

If you have any questions you can call our office at 717-898-3278, or EMAIL is at almtaxbill@comcast.net.

Click above to visit this IRS site.

Internal Revenue Service

DO YOU OWN SERIES EE OR I SAVINGS BONDS? Do you have savings bonds that have matured and stopped earning interest? It is important to check your savings bonds to see if they are still earning interest. How long savings bonds earn interest depends on the issue date. Series E bonds, issued from May 1941 through November 1965, earned interest for 40 years. If you own any Series E bonds, they are no longer earning any interest. Bonds issued after November 1965 mature in 30 years. Series I bonds mature after 30 years. Lost or misplaced bonds can be reissued by filling out Form PD F 1048.

Series EE Bonds

Series EE bondsreplaced the Series E bonds in 1980. Both these bonds were traditionally issued as a paper bond but can now be purchased in electronic form. Paper bonds were sold at a discount, and the difference between the redemption value and purchase price is the interest. Series EE must be held for a minimum of one year; there is a penalty of three months interest, if redeemed during the first five years. The method for calculating the interest on savings bond has changed several times.

Taxability of Interest

Interest on savings bond is subject to federal income tax, but not state income tax. Who is responsibility for paying the tax on these bonds? If a bond is purchased with one name on the bond, that person is responsible for the tax. If a taxpayer buys a bond with a co-owner, the person whose funds bought the bond is responsible for the tax. If two persons buy a bond as co-owners with each contributing the purchase, both owners are responsible for the tax in proportion to the amount paid.